While domestic debt remains a large share of Nigeria’s rising debt, there has been a growing reliance on external loans from private and bilateral creditors that are yet to put forward debt relief programmes since the pandemic began. Across Africa, there is a looming solvency crisis.

In November of 2020, Zambia became the first African country to renege on its debt service obligations since the COVID-19 pandemic began. Since then, official and private lenders as well as governments have become apprehensive about a looming solvency crisis in Africa. This heightened perception of risk is underpinned by the fact that like Zambia, most countries on the continent are commodity-dependent and have borrowed considerably from lenders that are reluctant in providing debt service suspension. Worse still, they are also experiencing a reduction in external financing from foreign direct investment, remittances, and development aid.

The debt sustainability analysis by the IMF and World Bank put forward in October 2020 shows that 16 countries in the region are already in debt distress or facing high risks. However, for some countries like Nigeria, debt as a share of GDP is relatively low – estimated at 35% in 2020 – leading to optimism in debt servicing expectations.

But debt expectations can change rapidly. The expectation that these countries will continue to service their debt, amid worsening economic fundamentals, may not be met. A sudden event such as a second wave of lockdowns due to African countries being left behind in accessing vaccines can very easily cause interest rates to increase unexpectedly and worsen future debt outcomes.

Moreover, acknowledging the possibilities of debt distress early on and planning for restructuring can reduce the duration of a debt crisis and output losses. Undoubtedly, there is an imminent debt-servicing problem not only for African countries but globally. Although the dimensions of the problem continue to evolve and, in some cases, could be unforeseen, this article examines the evolution of key economic indicators and policy responses in order to assess the likelihood of a brewing debt crisis and the possibility of debt restructuring in Nigeria.

Also Read: Private Creditor Debt Relief Will Deter Capital Flow to Africa, says Rencap’s Roberston

The Current Situation

While domestic debt remains a large share (58% in 2019) of Nigeria’s rising debt, there has been a growing reliance on external loans from private and bilateral creditors (see Figure 1) that are yet to put forward debt relief programmes since the pandemic began. Although the country is eligible for the Debt Service Suspension Initiative (DSSI) which suspends debt service payments on loans from G-20 countries until June 2021, the possibility of being deemed credit-unworthy by creditors has made the government unwilling to participate in the DSSI. As such, external debt service payments continue to be made with national estimates putting total disbursement from January to September of 2020 at US$1.26 billion.

However, bondholders in the domestic market have not been paid since August 2020 pointing to the severity of the liquidity crisis the country currently faces as the price of oil – which contributes 50% of consolidated government revenue and 80% of exports – has fallen considerably, and economic activities have not completely recovered since the period when the movement was restricted. The most recent estimates show that government revenue will decline from 8% to 5% of GDP between 2019 and 2020, with the chronic shortage of finance causing the Federal Government to spend up to 96% of revenue generated on interest payments in 2020. As a result, the government has sought US$3.4 billion from the IMF in emergency financial assistance which is yet to be disbursed.

An Emerging Downward Spiral

Aside from the unwillingness to service domestic debt, initial signs of an impending sovereign debt crisis are beginning to appear as bond spreads continue to widen considerably, pointing towards anxiety from investors. As of this writing, spreads between short-term and long-term bonds (2-year vs 10-year bonds) have peaked to 556 basis points relative to 217 basis points (see Figure 2) in March of 2020 – before the pandemic’s disruption to the economy. This anxiety is fueled by acute foreign exchange shortages, earlier alluded to, which has led to the Central Bank of Nigeria (CBN) adjusting both the official and the Investors and Exporters (I&E) exchange rate. Already, the latter exchange rate which is a more market-determined exchange rate for investors, exporters, and end-users has been revised downwards on three occasions since the pandemic began – March, August, and November 2020 – from NGN307/US$1 to NGN410.25/US$1 further undermining the government’s ability to cover its external financing obligations.

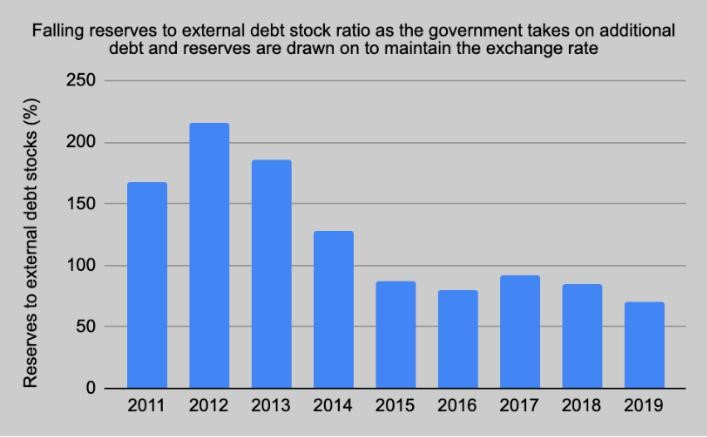

Even so, the exchange rates are still not market-determined as indicated by a wide parallel market premium and could be devalued further should negative oil price volatilities persist. This development is reflected in the drawing down of already declining reserves, as total reserves as a share of external debt stock has more than halved between 2013 and 2019 (see Figure 3), and poses vulnerability concerns amid the uncertainty of accessing capital markets until the crisis recedes.

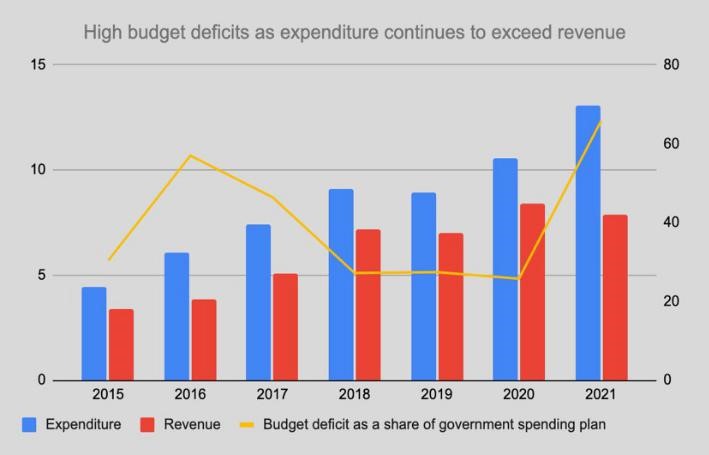

Meanwhile, there appear to be no signs of fiscal consolidation as the budget deficit as a share of the government’s spending plan which was already high averaging 36% between 2015 and 2020, is projected to peak to 66% in 2021 (see Figure 3). The increased spending is targeted at social protection and poverty reduction programmes, as well as sectors expected to aid a post-COVID-19 economic recovery. While the budget is unlikely to be completely implemented as indicated by historical precedents, the large spending plan together with the exchange rate volatility and the implication on debt servicing capacity has set off a confidence crisis.

The perceived risk of default could be self-fulfilling taking into consideration the trend and impact of other economic indicators and policy responses on the debt dynamics. Interest rates on Nigerian bonds are at historically low levels causing the government to borrow more cheaply amid an already constrained fiscal space which can contribute to the underpricing of risk and taking on larger-than-sustainable debt. For instance, the Debt Management Office’s December 2020 bond issuance valued at NGN60 billion (US$ 157.9 million) was oversubscribed by NGN74.056 billion (US$194.7 million).

Also Read: Financing Nigeria: Unlocking Liquidity Crucial to Fueling Development – Dr. Ayo Teriba

Bearing in mind that growth rates are unlikely to recover in the near term, a large debt stock will become more difficult to sustain. More so, with the CBN rolling out a number of credit guarantee schemes to the private sector, the increase in contingent liabilities during an economic downturn may very well turn into actual liabilities. Presently, the CBN guarantees at least 16 financing interventions cutting across multiple sectors including agriculture, entertainment, and manufacturing, and has disbursed NGN434.8 billion (US$1.14 billion) in the first half of 2020 alone.

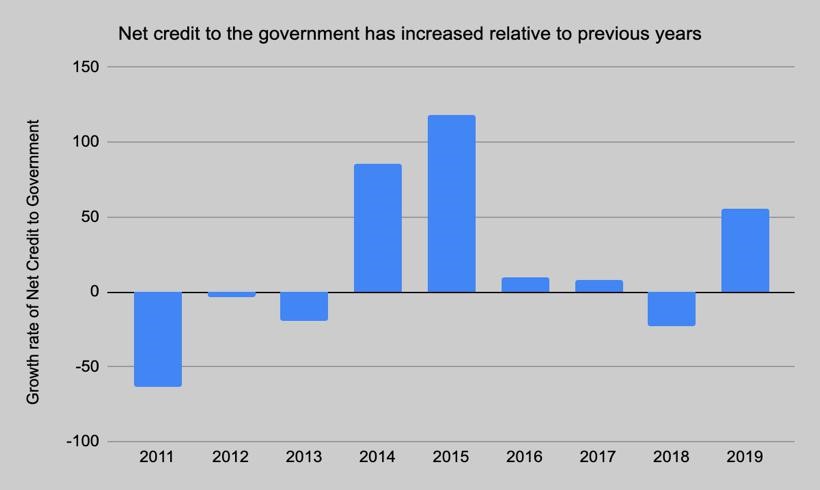

These guarantees alongside the CBN increasingly financing government purchases can speedily lead to large increases in debt levels. As indicated in Figure 4, the growth rate of net claims made by the CBN on the federal government grew by 55.8% to NGN7.58 trillion (US$19.95 billion) in the first half of 2019 relative to negative growth rates recorded between 2011 and 2013. While financing the fiscal deficit is within the legalities of the CBN, it creates a moral hazard problem. With a buoyant central bank, the government has little incentive to reduce the fiscal deficit and efficiently manage spending as it can find recourse in the CBN. As such, the increase in public spending and reduction in revenue as a result of the pandemic makes the central bank even more vulnerable to increased financing of fiscal deficit which could further worsen debt outcomes.

Looking Ahead

The current liquidity constraints amid the adoption of an expansionary fiscal policy underscore the need to immediately free up resources. Although participation in the DSSI may signal credit unworthiness to lenders and increase interest rates on loans, non-participation appears to be having a similar outcome as the inability to meet financing obligations has led to major rating agencies downgrading the country’s credit rating to highly speculative regions. Consequently, the cost of abstaining outweighs the US$123.5 million in DSSI savings which can curb the urgency to borrow particularly at non-concessional terms. Aside from creating additional fiscal space, these funds will also mitigate the need for further currency devaluations.

At this time, excessive currency swings will have a debilitating effect on debt servicing requirements and risk assessment. The CBN can activate swap lines with the central banks of currencies in which Nigeria owes a large share of its debt. In 2018, Nigeria and China entered a currency swap agreement which can be drawn on to expand foreign currency resources given the level of debt owed to China. Making the case to establish a swap line with the Federal Reserve as has been done by other emerging economies such as Korea and Brazil may be considered, as concerns regarding the sustainability of Nigeria’s external debt are largely due to the COVID-19 pandemic. Such arrangements will reduce currency depreciation pressures, stabilize the foreign exchange market, and is in the interest of investors and creditor countries.

Also Read: We Can’t Breathe: How African Countries Suffocate Themselves With Debt

More so, the drastic increase in budget allocations for sectors essential to economic recovery poses unrealistic expectations in budget execution particularly as it is occurring in the context of historical underspending in government budgets. While the unforeseen economic crisis has necessitated the use of new Public Financial Management (PFM) arrangements including CBN loan advances and drawing on reserves, excessively drawing on these buffers will have dire implications on inflation and increase the vulnerability to external shocks. Using more realistic assumptions for revenue projections will better guarantee financing for essential services as key sectors such as health and social protection, and capital expenditure is typically more disproportionately affected by unmet expenditure.

In the spirit of preparedness, determining how much debt restructuring is needed – based on a multiple scenario debt sustainability analysis – is of utmost importance. The narrow revenue sources for the government together with the wide range of loan terms offered by its diverse group of creditors, emphasizes the significance of mapping out debt service payments within the current revenue capacity. Rather than default in a worst-case scenario, this analysis can be put forward to creditors at an earlier stage and can be a starting point for negotiations. Debt swaps – the exchange of debt for the local currency which can be invested in the home country – can also be leveraged on. A large share of external debt is owed to multilateral creditors who in the past offered Nigeria a reduction in debt for investments in poverty alleviation efforts under the Multilateral Development Relief Initiative (MDRI). Such arrangements can be made as the government utilizes the high debt levels as an opportunity to finance its economic and sustainability agenda.

This article was first published on the website of the Center for the Study of the Economies of Africa, one of Africa’s leading think tanks based in Nigeria. Written by Mma Ekeruche, a Research Fellow at CSEA.