There are growing concerns about Nigeria’s fiscal situation. Key sources of concern are the country’s dwindling revenues, soaring deficits, growing debt levels, and escalating debt burden. These led the International Monetary Fund (IMF) to urge the government “to lower the ratio of interest payments to revenue and make room for priority expenditure” during its March 2019 Article IV Consultation with Nigeria. Some local and foreign media organisations and commentators have also raised questions about Nigeria’s solvency.

Nigeria urgently needs to address three main types of illiquidity, if the country is to fully come to grip with its persistently low financing thresholds. Development finance plays a crucial role in this context by mobilizing the necessary resources to support fiscal, financial, and foreign exchange liquidity thresholds.

The three types of illiquidity challenges – fiscal, financial, and foreign exchange – are each analysed in turn in the following sections.

- Fiscal liquidity threshold

From a development finance point of view, there are three thresholds of fiscal liquidity that government revenue should meet, namely:

- Recurrent spending (salaries, overheads, and debt service/interest payments)

- Capital spending

- Debt repayment and/or rainy-day funds – fiscal buffers

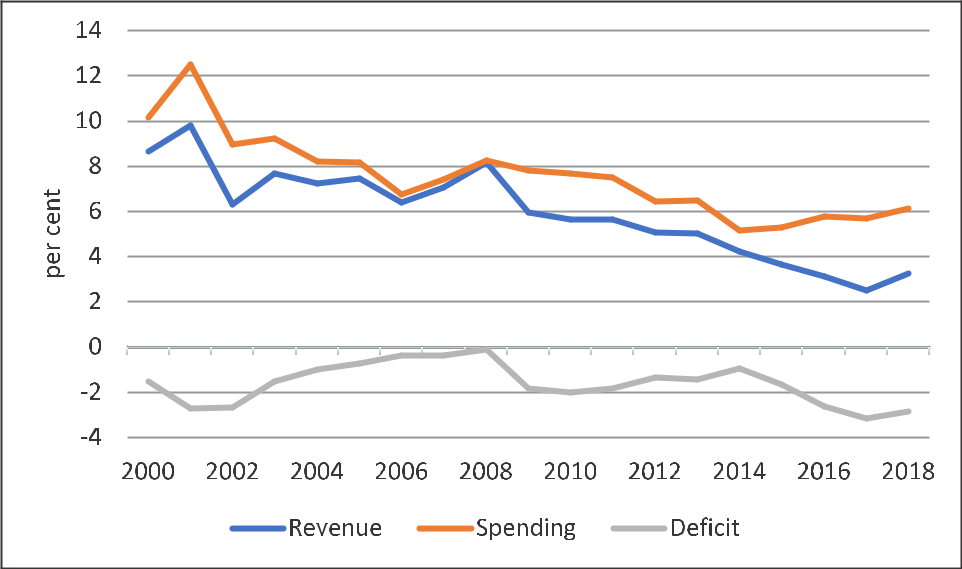

At well below 10% of gross domestic product (GDP) since 2015, the total revenue available to the three tiers of government has fallen so low that it does not even cover the recurrent spending threshold of fiscal liquidity, as salaries and debt service each amounted to 70% of federal government revenue in 2017. Deficits had to be incurred to meet both in full, with additional borrowings to meet shrinking overheads and a small and contracting capital spending. With less access to debt markets, many states were unable to meet their salary obligations in full, creating unpaid arrears of more than 12 months in some.

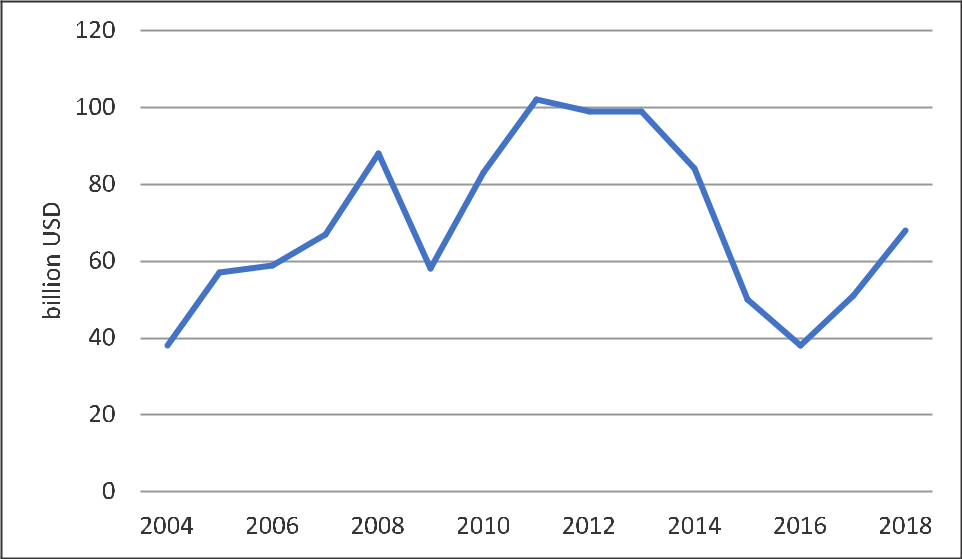

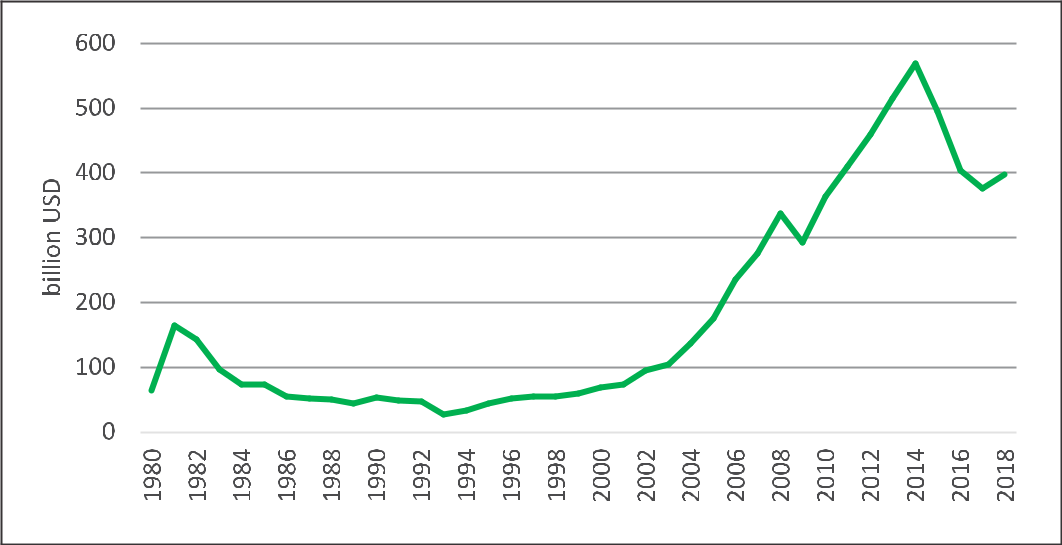

Oil exports and taxes are the main sources of government revenue in Nigeria. The oil price’s weakness since July 2014 and oil output losses have combined to see annual export earnings in the country fall from an average of almost $100 billion in 2010-2014 to less than $50 billion since 2015, with strong negative implications for government revenue. Concomitant bouts of growth reversal and devaluation since 2015 have eroded corporate profits and household incomes, with adverse implications for tax revenues. Leveraging development finance instruments like infrastructure bonds and sovereign wealth funds can provide the necessary capital to bridge the fiscal gap.

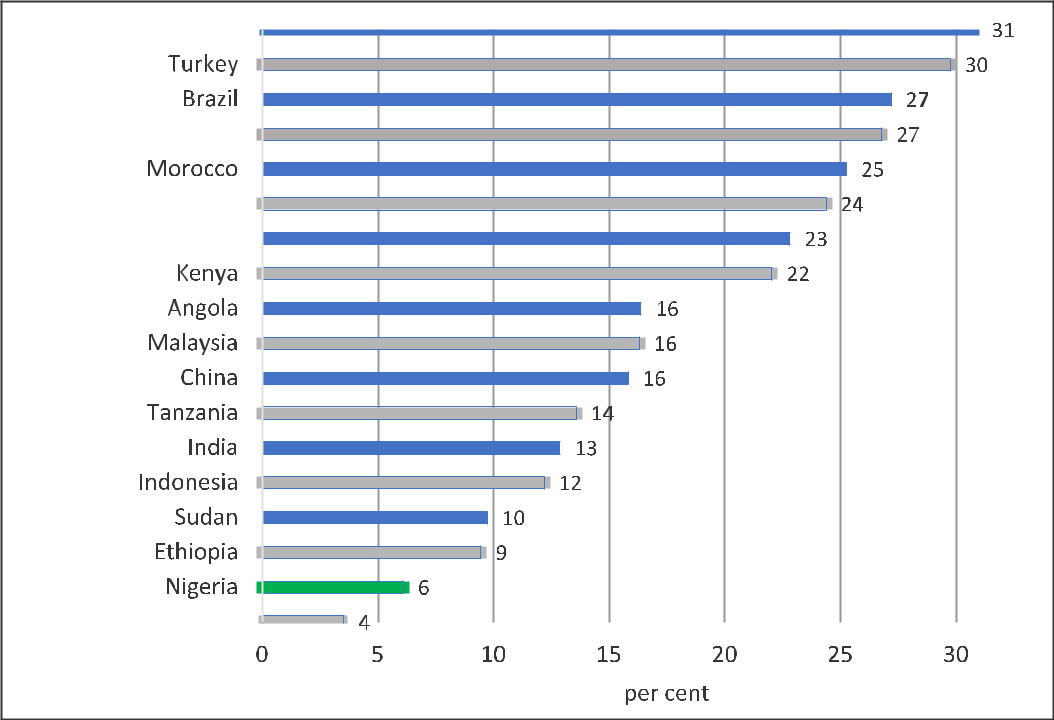

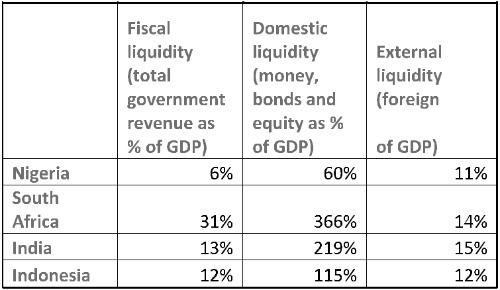

The Nigerian government must find ways of opening new streams of non-export and non-tax revenue to cover the higher thresholds of fiscal liquidity. Most of Nigeria’s peers currently have total revenues that range between 15% and 30% of their GDP, compared to about 6% or 7% of GDP in Nigeria, and therefore are able to meet much higher thresholds of fiscal liquidity. As mentioned earlier, many of them have achieved this by opening new non-tax revenue streams that flow from optimising national assets. Nigeria’s peers include BRICS (Brazil, Russia, India, China, and South Africa), MINT (Malaysia, Indonesia, and Turkey), African countries with a GDP of $50 billion or more, and Saudi Arabia and the United Arab Emirates in the Middle East.

- Financial liquidity threshold

Domestic financial markets in Nigeria remain shallow, meeting only basic transaction needs. Development finance institutions (DFIs) can play a significant role in improving financial liquidity by providing long-term funding and investment opportunities. Nigeria’s financial system must meet three thresholds:

- Transactions or payments threshold

- Precautionary or savings threshold

- Speculative or investment threshold (domestic money, bonds or equity buffers)

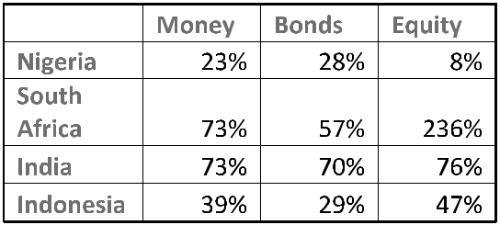

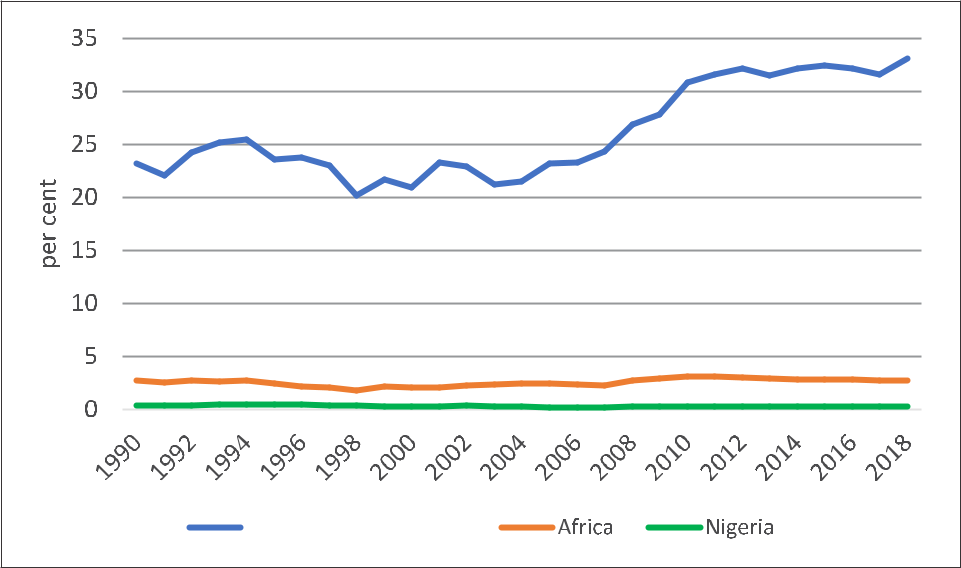

Nigeria meets only the lowest threshold of domestic financing, as the funds at the disposal of domestic banks can only meet transactions or payments needs, meaning that they do little more than honour demands for cash and e-payments at points of sale and domestic fund transfers (which they do remarkably well). Nigerian banks disappoint when it comes to extending loans, as the total deposits at their disposal are so low – around 20% of GDP – that they do not have the necessary funds. This effectively makes them financial intermediaries in name only. In peer countries, bank deposits are 40-200% of GDP.

Capital market reforms and access to Development Finance Institutions can enhance the availability of long-term financing, allowing businesses and households to participate more actively in the financial system.

The weak naira also hampers the development of domestic financial markets. Development finance strategies that stabilize exchange rates can help attract investors to naira-denominated assets, promoting deeper markets and greater financial inclusion.

Nigerian bond and equity markets are just as shallow as the banks, with the result that access to these markets is restricted to the biggest issuers. The government dominates the bond market (raising alarm about the cost of accessing bonds) and increasingly issues foreign bonds that offer much lower rates; and the biggest companies dominate the equity market. Nigeria’s peers have deeper banks, bonds, and equity markets that offer access to low-cost financing for government, companies, and households.

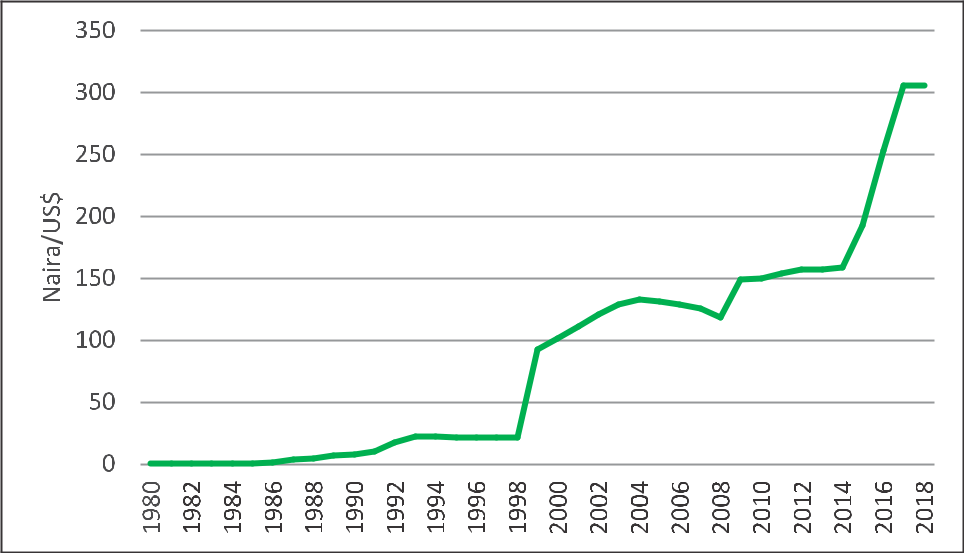

The weakness of the naira relative to the US dollar and other currencies is the main reason why Nigerian banks and bonds, as well as the equity market, are shallow. Assets denominated in a weak currency will be poor stores of wealth, and asset holders will be better off holding hard currency or real estate than keeping wealth they do not require for transactions in naira-denominated bank deposits, bonds, or equity.

- Foreign exchange liquidity threshold

There are three thresholds of external liquidity that foreign exchange markets or the national foreign reserves holdings should meet for the market and the exchange rate to remain stable:

- Transactions or external payment threshold

- Precautionary or insurance threshold

- Speculative or investment threshold – foreign reserve buffers

With foreign reserves at 10.8% of GDP, compared with 20% of GDP or more in many of its peers, Nigeria struggles to meet the transactions or external payment thresholds defined to include trade obligations, such as payments for imports, and financial obligations, such as short-term external financial claims on households, businesses, and financial institutions. Development finance solutions, such as attracting foreign investment and remittances, can enhance foreign exchange reserves, supporting long-term stability.

The foreign exchange at Nigeria’s disposal cannot meet transaction demands, and the central bank has adopted various methods to exclude a growing number of lawful buyers from the market since 2014, resulting in a multiplicity of exchange rates. Despite this, the naira has lost nearly two-thirds of its value against the US dollar over the past four years to reflect the forex market’s illiquidity.

As Nigeria struggles to meet the lowest threshold, any unforeseen shock that requires precautionary reserve holdings, such as a shock to its export volume or export price or a shock to capital outflows, will push the country and the naira into another tailspin for as long as the shock lasts, just as any opportunity that requires the deployment of speculative reserve holdings cannot be seized.

Thus, the country’s perennial external illiquidity crisis is the bane of the weak naira, and the weak naira is in turn the bane of the shallow banks, bonds, and equity market, and shallow domestic financial markets are the reason for growth reversals.

Understanding the growth-stability-liquidity nexus

External liquidity is key for an economy of Nigeria’s size and profile. Since the early 1980s, the country has struggled with growth because of domestic illiquidity, whilst also contending with exchange rate stability because of external illiquidity. Policymakers need to recognise that, unless liquidity concerns are addressed, growth and stability aspirations will remain elusive. The 2004-2008 growth acceleration episode in Nigeria was fuelled by a surge in its external liquidity as a result of steady increases in the price and volume of oil exports.

The period stands out in Nigeria’s post-1980 history as the only time the naira appreciated, the banking system, bond market, and equity market deepened markedly, and growth accelerated. Such was the magic of adequate external liquidity. Nigeria must thus ensure adequate internal and external liquidity to restore growth and stability. The sequencing is crucial: external liquidity is required for exchange rate stability; exchange rate stability is required for domestic liquidity; and domestic liquidity is required for growth.

Nigeria must reorder its economic policy priorities to: External liquidity → exchange rate stability → domestic liquidity → growth Stimulating enough foreign capital inflows is key for stability; getting business done, even when business is easy to do; the rebuilding of infrastructure; growth acceleration; growth diversification; and generating employment, wellbeing, and prosperity to underpin inclusive security.

As Joseph Joyce demonstrated in 2018, over many years Nigeria’s peers have learned to deepen external liquidity, stabilise the exchange rate, deepen domestic liquidity, and grow the economy, with external liquidity as the silver bullet (see table 2 above). The other three – exchange rate stability, domestic liquidity, and growth acceleration – will happen automatically once the steps needed to boost external liquidity are implemented effectively. This is evidenced by Nigeria’s 2004-2008 external liquidity surge, exchange appreciation, financial deepening, and growth acceleration.

Opportunities for unlocking liquidity

At least three factors currently are all favourable for unlocking the liquidity that the Nigerian economy urgently needs. These include the global liquidity glut, the opportunity to join the emerging market economies’ race for the global liquidity glut, and opportunities for domestic public wealth conversion. Each of these is analysed below:

- Opportunities offered by the global liquidity glut

The global liquidity glut offers unprecedented opportunities for Nigeria to attract easy capital inflows to stabilise the naira, deepen domestic liquidity, and fuel growth.

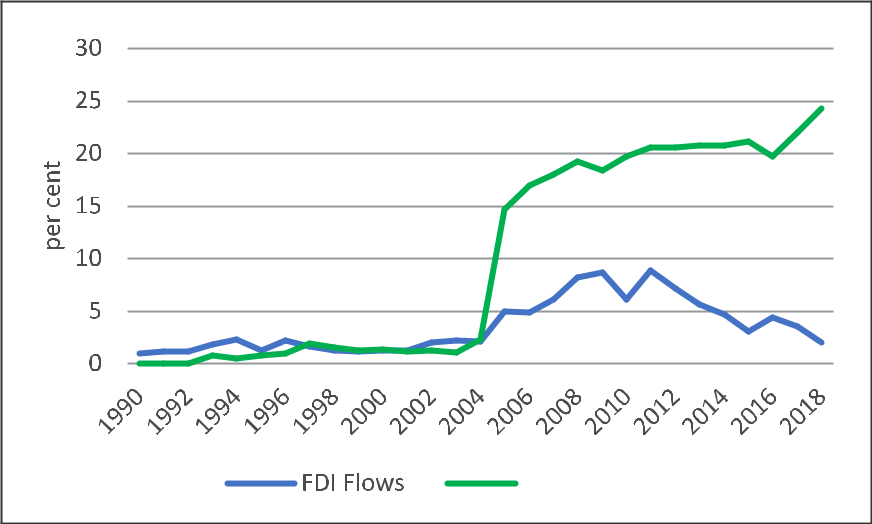

Annual inflows of foreign direct investment (FDI) and diaspora remittances into developing countries now exceed a trillion US dollars, but these are concentrated in a few developing countries that have adopted investment-friendly policies. Nigeria is not on that list, as its shares of both types of inflow have been on a steep downward trajectory even as these flows have doubled over the past decade and a half.

2. Opportunities to join emerging market economies’ race for global liquidity

It is imperative that Nigeria joins the shortlist of developing countries that are getting increasing shares of both FDI and remittances as these flows continue to surge. Unfolding global realities mean that Nigeria could easily adopt policies that would raise external liquidity thresholds enough to switch from contraction to expansion. The country must join the race for massive private-to-government remittances from non-resident citizens and narrow the gaps between itself, China, and India.

Nigeria’s peers like Egypt, India and Saudi Arabia, and other emerging markets are taking full advantage of the opportunities to deepen external liquidity, stabilise their currencies, and deepen domestic liquidity to fuel growth, infrastructural development, employment, and poverty eradication. In the mid-1990s, Nigeria had larger stocks of FDI than India, Saudi Arabia, or the United Arab Emirates, but these have all since overtaken Nigeria. India now has more than triple, and Saudi Arabia more than double, Nigeria’s FDI stock.

- Opportunities for domestic public wealth conversion

Despite the negative external income shock, the domestic reality is that Nigeria remains prodigiously asset rich. However, while its economic and financial struggles resulting from the decline in income have been prominent in economic news headlines, the value of assets owned by Nigeria and the solutions these assets could unleash have been less highlighted. It is time to pay attention to the hidden value of these assets and unlock the considerable domestic and external liquidity needed to arrest Nigeria’s extant economic and financial crisis.

Options for unlocking liquidity

The following four options could raise domestic and external liquidity thresholds in Nigeria:

- Securitise (not sell) equity holdings in Nigeria Liquefied Natural Gas (NLNG) and other oil and gas joint ventures to give Nigerians at home and in the diaspora the opportunity to invest in these assets and earn some of the dividends.

- Privatise to attract brownfield FDI by converting all wholly-owned corporate assets into securitisable joint venture stakes in which the government owns up to 49%, privatising (selling) the rest to allow foreign investors to own a minimum of 51%, like the NLNG.

- Liberalise to attract greenfield FDI by breaking the government’s monopoly on infrastructure to encourage the entry of foreign investors operating in parallel to joint ventures.

- Commercialise idle or under-utilised government-owned land and built structures by leasing (not selling) them, relocating uneconomic activities from prime locations, and repurposing such locations for leasing, to open new streams of lease/rental income into government coffers.

Doing all these will change Nigeria’s economic, fiscal, and financial narratives by unlocking vast amounts of liquidity to strengthen the naira, rejuvenate fiscal, financial, and foreign exchange streams. The new liquidity will also help to rebuild infrastructure, diversify and accelerate growth, eradicate poverty and unemployment, and lay the foundations for shared prosperity. Leading developing countries such as China and India adopt different combinations of the four options to fuel their development. Nigeria’s high population, scattered across hundreds of densely populated cities, combined with the recent oil boom, have bequeathed the country with valuable but idle public assets that can be unlocked to raise much-required liquidity.

About the Contributor

Dr. Ayo Teriba is the CEO of Economic Associates (EA), a research and consulting firm specialized in the Nigerian economy with a focus on global, national, regional, state, and sectoral issues. He is the Vice-Chairman of the Technical Committee of the National Council on Privatization (TC-NCP) and is a Member of the Board of Economic Advisers in the Office of the Economic Adviser to the President. Ayo has served as a Consultant to many blue-chip companies, a host of federal ministries, departments and agencies, numerous state governments, DfID, USAID, UNIDO, and the World Bank. He was a visiting scholar at the IMF Research Department in Washington DC. Ayo earned a B.Sc. in Economics from the University of Ibadan, MPhil in Economies of Developing Countries at the University of Cambridge, and a Ph.D. in Applied Econometrics and Monetary Economics from the University of Durham. He is an Alumnus of the Lagos Business School (AMP 5) and the Henley Business School (BDP) Executive Programme.

This article is a contribution to the inaugural edition of Nigerian Governance Insight.

2 Responses