This a detailed read on the CBN’s poor communication of issues and its costly policies. The first section traces CBN’s poor crisis management between 2015 and 2017, which is similar to its COVID-19 response. The last section focuses on its weak response to the NESG in light of the institutions’ recent publication on issues facing the Nigerian economy. Skip to the sections you want. Pardon errors, rushed and unedited.

Earlier in the year, when the impact of COVID-19 was becoming evident, I wrote a thread on how the biggest challenge facing us would be CBN’s communication problem and policies. I have been mostly correct.

This prediction was not because I was smart or could see the future. It is simply what you expect from a Bank that has left a trail of communication failings in its wake in the past five years. History might not the best predict the future, but with the current CBN, the thinking seems stuck in the past with no room for new learning.

The CBN said there would be no devaluation only to devalue some days later. The Bank has also attacked importers, exporters and BDC operators. This is a playbook from the past and bad policies seem to be on a timeless loop.

A Communication Disasterclass between 2015 and 2017

Before I go into the CBN’s latest tantrums about NESG’s 15-point highlight of issues facing Nigeria, let me talk about the trail of CBN’s communication problems during the last crisis between 2015 and 2017.

- In February 2015, Premium Times talked about the widening premium at the parallel market after the devaluation in September 2014 was below market expectation. The paper also wrote about how foreign investors, in this case, JP Morgan, complained about illiquidity in the FX markets that deterred the entry and exit of foreign investors. JP Morgan had threatened to delist Nigeria from its index, which emerging market investors looked at before making decisions. The CBN responded to both issues, it was important to do so due to capital flows. The CBN Governor stated that the Bank would do everything possible to prevent delisting. In the same month, the CBN devalued from N169/$ to N197/$.Post-2015 elections and after two devaluations (November 2014 and February 2015) driven by the oil price crash in mid-2014, the CBN later decided that a devaluation was a bad thing to do. In the linked article, the position of the President and Vice-President, people who should have no control over monetary policy, was used as justification by the CBN. This reduced liquidity in the market and the Bank implemented capital controls (policies that made it difficult for investors to bring in USD and exit).Much later, JP Morgan eventually delisted Nigeria. In classic fashion, the CBN which took measures to prevent an exit, worked with the DMO to release a bombastic circular on how that delisting meant nothing and would have no impact. Much later, the impact would be seen in the record moderation in capital importation into Nigeria as foreign investors turned away. The only other time Nigeria has had worse investment numbers is this year, no thanks to COVID-19 and the CBN’s poor response.As economic conditions worsened despite the CBN talking down a devaluation, blaming speculators and importers, sponsoring tweets to attack analysts on Twitter and cutting down trees to stem the fall in the currency, the Bank eventually devalued mid-2016 and in early 2017. In early 2017, the CBN created the I&E window to entice foreign investors that they claimed did not matter less than two years earlier. Between 2017 and 2019, the CBN destroyed its balance sheet by selling securities to this same foreign investors to attract USD flows.

From going against a devaluation and peddling myths against a devaluation, the CBN adjusted from N197/$ to N365/$ in two years. All along the way, communication was poor and inconsistent and the consequences were dire. Doctors are some times jailed for malpractice, not policymakers who spread poverty and destroy businesses.

CBN’s Tantrums at NESG’s Take on Recent Economic Challenges

Now to the important issue. I am sure most of us have read the NESG’s take on recent issues in Nigeria. This was a very measured consideration of issues facing Nigeria and I am surprised by the CBN’s sensational reaction which would be hilarious if not sad. The quality of the response and the language were disappointing, to say the least. In the following paragraphs, I will walk you through the CBN’s poor understanding of issues and deliberate misrepresentation of facts.

On Weak Growth and CBN’s COVID-19 Response

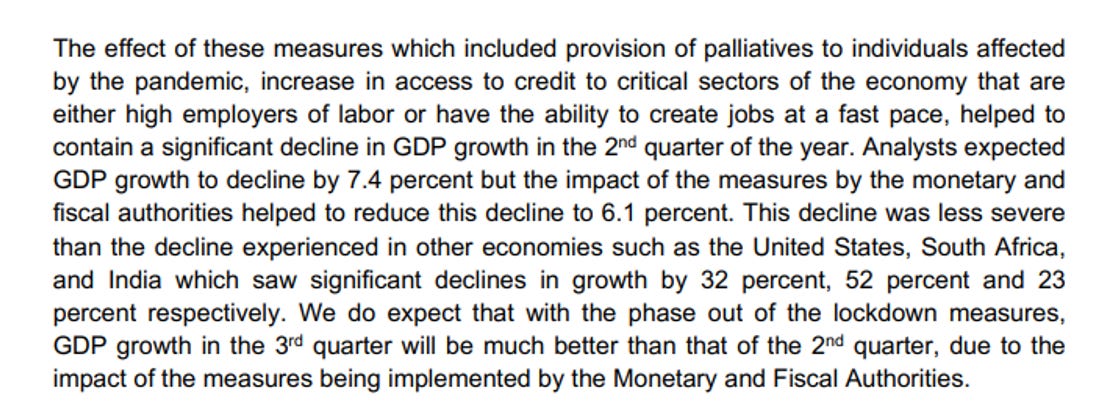

Below is what the CBN has to say on the performance of the economy. The major point is that the CBN claims to have staved off a worse performance unlike in India, US, and SA.

The CBN says analysts expected a decline in GDP of 7.4% in Q2 but the actual was better at -6.1% due to their measures. This is hilarious because the same CBN expected (PDF: Page 3, last second to the last paragraph) a contraction of just 1.03%. So why is the CBN praising itself for a contraction of 6.1% when they expected a decline of just 1.03%?

Also, the CBN tried to imply that Nigeria did well because SA’s GDP declined by 52% in Q2. What the CBN did not mention was that SA calculates its growth numbers differently. If you assume the same methodology as Nigeria’s, SA’s performance was a decline of around 17%, still bad but obviously way off 52% innit?

Finally, it was convenient that the CBN chose countries doing much worse. There are countries likely to have outperformed Nigeria in Q2 – peers such as Ghana, Kenya and Egypt.

On CBN’s COVID-19 Disbursements

The CBN claims that its development finance activities are felt by Nigerians and the justification provided is hilarious.

You don’t need to be smart to see this as pure nonsense. Who takes credit for disbursing N59.1bn to households and businesses in a country where consumer spending is N107.7tn annually and the contribution of SMEs exceeds 50% (over N70.0tn) of GDP? The Bank’s intervention is clearly too negligible to have an impact, nice try though.

On the Inadequacy of Monetary Disbursement to Farmers

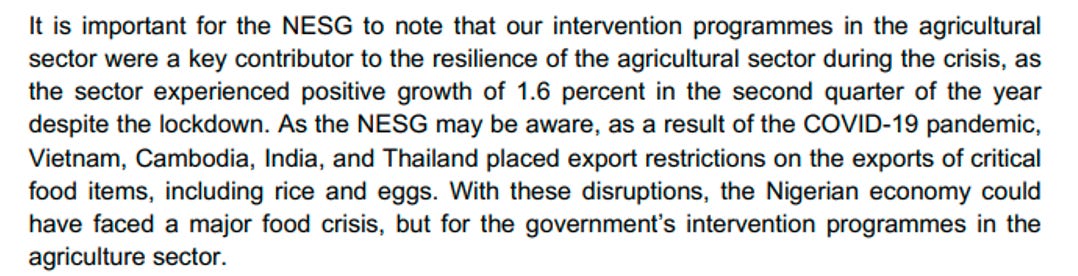

At this point, I am convinced the CBN operates in an alternate reality. The Bank is claiming that its intervention programmes have ensured that Nigeria is not facing a food crisis.

This shows the CBN is disconnected from the reality of the average Nigerian, nor do they take notice of facts available. The latest price watch of the NBS (see image below) as of July 2020 shows that Nigeria is indeed in the middle of a food crisis. Or how else do you justify these price changes over a one year period? Food insecurity in Nigeria is similar to what is obtainable in war-torn countries, I wrote about it here a year ago. It’s getting worse. One would expect a CBN with an inflation target of 6-9% to know better in a country where inflation is 12.8% and rising.

On the Quality of CBN’s Development Finance Activities

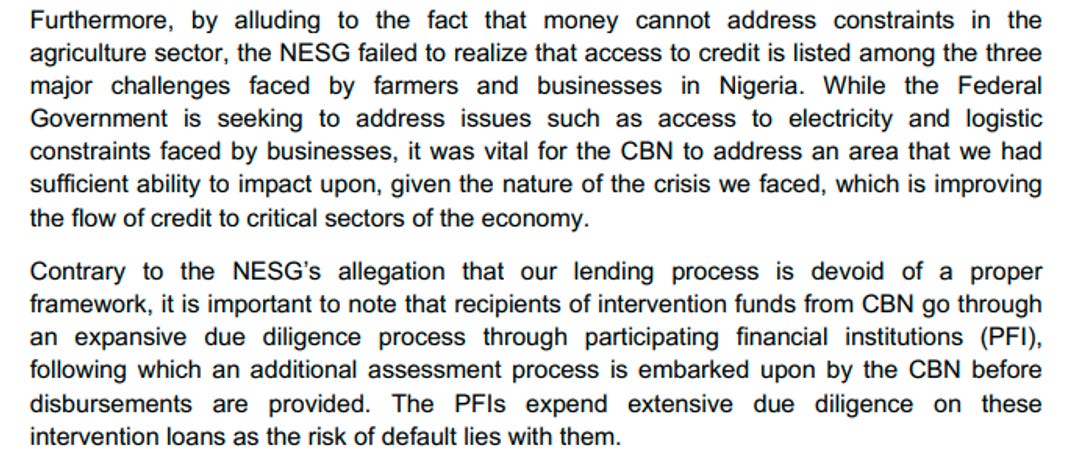

The Bank made a fair point in stating that one way in which it could support farmers was in the area of funding. However, what makes the Bank think it’s interventions are working if other critical issues have not been resolved? Why are they using money to fix a multifaceted problem and then claim the credit? Just last week Bloomberg reported that floods have wiped off around 25% of rice harvest.

On NESG’s claim that the lending process is not ideal, the CBN noted that there was adequate due diligence and pricing of risk. This is not honest. Many farmers claim not to have received disbursement. Some complain that disbursement is usually slow and after the planting season. And for those with access, the farmers have failed to repay back the loans disbursed under the Anchor Borrower’s Programme, for instance. Premium Times, Business Day and Guardian have all reported it extensively. So why is the CBN claiming that it is a successful programme when loans are not properly disbursed and they are mostly not repaid?

Beyond agriculture, even the COVID-19 support offered to businesses and households through Nirsal was disbursed through a poor lending process. There are beneficiaries who allegedly never submitted complete documents but received credit alerts! There is a problem with the CBN’s approach to development financing and there is no evidence that it works.

On Trade and Border Closure

I am not surprised that this is the best response the CBN could provide for the extended closure of borders which has had devastating consequences. It is hard to defend poor policies.

In an economy with needs for new sources of FX other than from oil, why is it reasonable to ban exports to neighbouring countries? When did it become economic sabotage to export products? A lot of Nigerian manufacturers have been affected by the closure of land borders, including those importing raw materials needed for finished goods that are exported.

Then why should the desire to block “harmful and illicit trade” affect “genuine” ones? In what planet does it make sense to impose a 70% tariff on a staple such as rice and also restrict FX for its import? Yet with all these anti-trade policies, if local rice production is still not competitive, shouldn’t this bring about a new approach?

What is clear is that it doesn’t make sense to create barriers to imports when domestic production is grossly inadequate. We have seen it with rice, it is also now evident with poultry products, as the CBN’s decision to stop selling FX to maize importers is creating problems.

The welfare impact of the border closure is well captured by this snapshot from the World Bank.

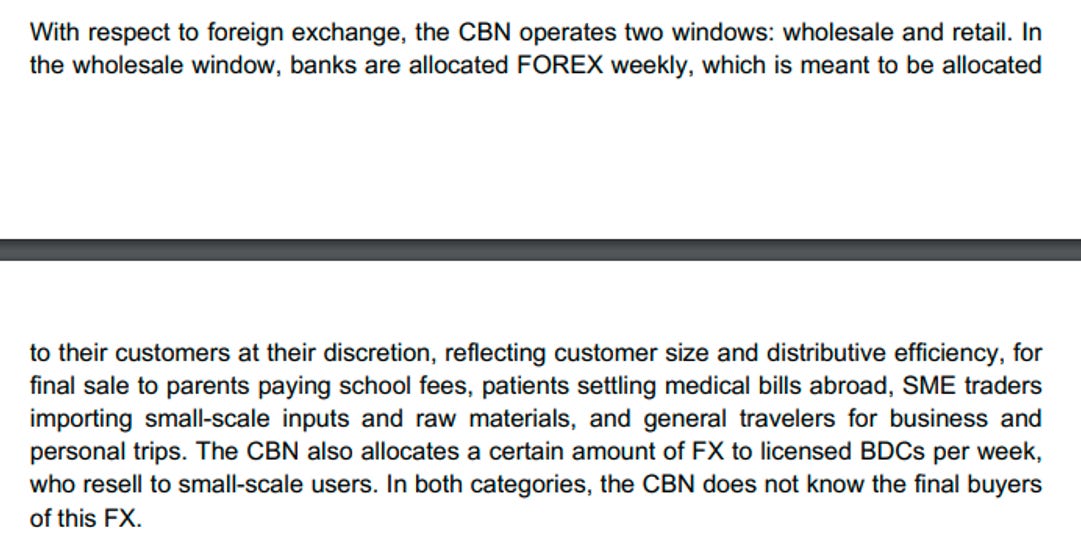

On the Lack of Clarity on FX, and poor FX Management

CBN’s management of the FX crisis has not inspired confidence. The failure to adopt a timely adjustment of the exchange rate in the face of reduced FX availability has resulted in a wide premium at the parallel market. The CBN also stopped sales to BDCs and the I&E FX window – what is supposed to be the market-reflective segment – since March 2020. In a market with weak supply and many prices (exchange rates) which create the room for arbitrage, it shouldn’t be hard to see how FX allocation would be inefficient and how economic activities would be disrupted.

On Interest Rate Management, Saving and Pensions

You won’t be wrong to think that the economists at the CBN with PhDs probably got their certifications by way of an affidavit with this response.

What the NESG alluded to was the challenges with low-interest rates or yields (treasury bills and bonds) in Nigeria, with rates on treasury bills around 2-3% and significantly below inflation at around 12.8%. In a country where the currency is losing value, this will result in loss of confidence and saving becomes less attractive to businesses and consumers. However, a high level of domestic saving is needed to boost investment and growth. Similarly, in a country with no safety nets, a negative real return (inflation > interest rates) would affect pension returns and the welfare of retirees in the future.

Yet the content of the above image is what the CBN offered as an explanation, redirecting the conversation to its recent policy which reduced interest rate on savings deposits. To be clear, the interest rate on savings deposits has always been poor relative to inflation. Before the latest change to 10% of MPR (the benchmark interest rate for the country) which is 1.25%, it was a minimum of 30% of MPR which was 3.8%. The rate was 4.2% between 2016 and 2020 when MPR was 14.0% while inflation averaged >13.0%. That clearly isn’t the point.

The CBN’s claim that because saving must equal investment, deposits must then be close to loans is a reach. The saving must equal investment equation, in theory, is for a closed economy. While our land borders are shut, we are not a closed economy. Saving in that context is also not the same as deposits, nor can loans be close to investment. Saving refers to the part of your income that is not consumed. If I borrow money from Wema Bank and deposit in GTB, does that count as saving too just because it is a deposit? Loans can be for all sorts of uses. It can be used to pay salaries, buy gadgets, purchase clothes, buy machinery, among other uses. But investment is actually spending on durable goods with uses beyond a year. How then should loans be close to investment?

Still on the Bank claims that total deposits should be close to total credit. Well, how will this be possible if the mandatory CRR (share of deposits kept with the CBN) is 27.5% while the actual CRR has recently surpassed 50.0% due to arbitrary debits?

This has been a long read and I am going to stop here. Clearly, the CBN chose to be sensational rather than react sensibly to the issues raised by the NESG. The CBN demonstrates a poor understanding of issues and tries to mislead with its response to the NESG. There were many other valid issues raised that were unaddressed. Without a doubt, competent people are needed at the CBN.

Adedayo Bakare is an associate at an asset management firm.

One Response