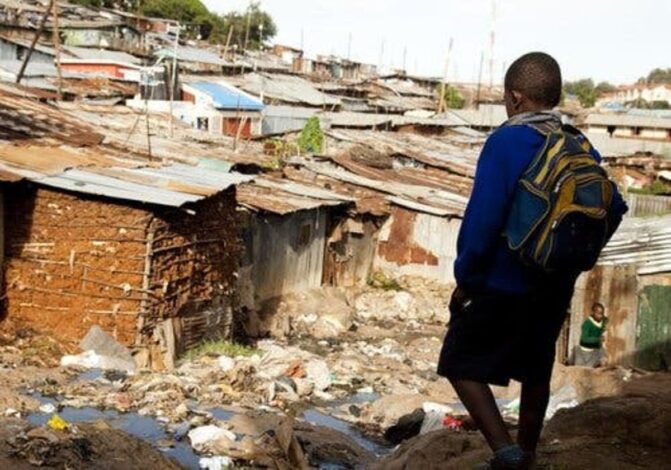

In a sobering revelation, the latest Nigeria Development Update from the World Bank estimates that 129 million Nigerians now live below the global poverty line—equivalent to 56% of the country’s population. This figure, released in October 2024, marks a sharp rise from the 40.1% reported in 2018. The report notes that between 2023 and 2024 alone, 14 million more Nigerians were pushed into poverty, underscoring the growing economic challenges facing the nation.

This alarming trend raises questions about Nigeria’s current economic policies and the ability of President Bola Tinubu’s administration to steer the country toward prosperity. As millions struggle to make ends meet, the debate intensifies over whether the government’s economic reforms, designed to stabilize a faltering economy, are working—or worsening the situation for the nation’s poorest.

The Economic Situation Before 2023: Policies in Decline

Before the current administration came into power in May 2023, Nigeria’s monetary and foreign exchange policies were widely criticized for being distortive and ineffective. The dual exchange rate system—where official and parallel markets coexisted with significantly different rates—was particularly problematic. This arrangement not only eroded investor confidence but also acted as a hidden foreign exchange (FX) subsidy, costing the Central Bank of Nigeria (CBN) significant revenue losses.

The petroleum subsidy regime also contributed to Nigeria’s fiscal problems. The Nigerian government spent approximately ₦400 billion ($500 million) monthly on fuel subsidies, an effort aimed at keeping fuel prices low for consumers. However, this spending consumed a substantial portion of oil revenues, reducing funds available for critical investments in infrastructure and social services. In 2022, the combined cost of foreign exchange and petroleum subsidies accounted for 5.2% of Nigeria’s GDP, equivalent to three-quarters of the revenue flowing into the Federation.

These policies led to large fiscal deficits, which were increasingly financed through “Ways and Means Advances” from the CBN—essentially emergency loans to the government. According to the CBN Act, these advances should not exceed 5% of the Federal Government’s revenue from the previous year.

However, by the end of President Muhammadu Buhari’s administration in 2023, the advances had ballooned to ₦23.8 trillion, overshooting the legal limit by 2,635%. This contributed to spiraling inflation and left 88.4 million Nigerians living in extreme poverty by the end of 2022.

The Tinubu Administration’s Economic Reforms: A Tough Road Ahead

When President Tinubu took office in May 2023, his administration immediately took steps to overhaul the economy. In his inaugural address, Tinubu made it clear that the long-standing fuel subsidy was no longer sustainable, stating unequivocally, “Subsidy gone.” By the evening of his swearing-in, fuel prices had surged from around ₦198 per liter to ₦500. This policy change, coupled with the decision to float the naira, caused a sharp rise in the cost of goods and services, fueling inflation, which by September 2024 had reached 32.70%.

Despite the immediate hardships caused by these policies, the government has also implemented key reforms that have shown signs of progress. Chief among these is the unification of Nigeria’s exchange rate, which has eliminated the parallel market premium and implicit FX subsidy. This, along with fiscal reforms such as rationalizing tax expenditures and improving revenue management, increased government revenues from 5.5% of GDP in the first half of 2023 to 8.7% by mid-2024.

The administration has also focused on ending deficit monetization and returning the CBN to its core mandate of price and financial stability. While these reforms are critical for long-term economic health, they have come at a steep cost for ordinary Nigerians, many of whom now find themselves deeper in poverty.

Economic Reforms Adding Strain to Nigerians

The removal of the fuel subsidy and subsequent rise in fuel prices have significantly increased the cost of living for all Nigerians, from low-income households struggling with soaring food prices to businesses grappling with higher energy costs. The depreciation of the naira following the unification of the exchange rate further exacerbated inflation, driving up the prices of basic goods and services.

Monetary policy tightening has led to higher interest rates, which have been particularly hard on micro, small, and medium-sized enterprises (MSMEs), reducing their ability to borrow and invest. For the poorest Nigerians, these economic strains have pushed many further into poverty.

A Worrying Trend: Nigerians Trapped in Unproductive Jobs

The World Bank report highlights not only the high levels of poverty but also the prevalence of “in-work poverty.” This means that many Nigerians, though employed, earn so little that they remain trapped in poverty. According to the report, around 75.8% of working-age Nigerians are employed, but many are in jobs that are neither productive nor remunerative enough to offer a path out of poverty.

Most troubling is the disparity between workers employed in larger firms and those in smaller businesses or self-employed. Workers in firms with 20 or more employees earn 71% more than those in smaller firms. However, the majority of Nigerians work in establishments with fewer than 20 people or are self-employed, limiting their earning potential.

Women and Youth at Greater Risk

The report also highlights the disproportionate impact of these economic challenges on women and young people. Women are less likely to hold formal, wage-paying jobs and are more often employed in lower-paying, informal sectors such as retail. Young Nigerians, despite improving educational outcomes, are more likely to be underemployed and working in jobs that do not make full use of their skills, limiting their ability to break free from poverty.

The Way Forward: A Call for Inclusive Growth

To reverse the worsening poverty situation, Nigeria must prioritize the creation of more productive jobs, particularly for its youth, who make up 70% of the population, and women, who are disproportionately affected by low-paying work. Investing in human capital development, especially in education and vocational training, is critical to equipping young people with the skills they need to succeed in an increasingly competitive job market.

Furthermore, policies must directly address the needs of the informal sector, where the majority of Nigerians work. Social protection frameworks should be strengthened to provide a safety net for the economically insecure, ensuring that ongoing economic reforms do not further impoverish the nation.

As World Bank Chief Economist Indermit Gill has warned, halting the current reforms would be disastrous. However, without additional measures to cushion the blow for the most vulnerable, the number of Nigerians living in poverty could rise far beyond the current 129 million, threatening the nation’s social and economic stability.