For more than a decade, Nigeria’s electricity crisis has been told as a story of weak distribution companies, politically sensitive tariffs and endless government interventions. But beneath the arguments over who owes whom lies a more stubborn problem: arithmetic.

Energy analyst Ebipere Clark has revived an uncomfortable question — whether the current debt resolution plan in the power sector actually adds up.

To understand the argument, one must strip away the policy language and return to basic cash flow logic.

How the Money Is Supposed to Flow

Nigeria’s post-privatisation electricity market is structured around a chain of payments. Generation companies produce power and invoice the bulk trader, the Nigerian Bulk Electricity Trading Plc (NBET), in naira. NBET then pays the generators, funded largely by collections from distribution companies and government-backed support mechanisms.

In theory, it is a straightforward commercial cycle.

In practice, it has never worked cleanly.

On average, GenCos receive only about 35 to 40% of what they invoice. The rest accumulates as arrears. Year after year, those short payments compound. What began as liquidity stress has hardened into what government now calls “legacy debt” — estimated at roughly ₦6 trillion owed to generation companies.

To tackle this backlog, the Federal Government has launched a multi-trillion-naira bond programme, reportedly valued at about ₦4 trillion, with an initial tranche already issued. The objective is clear: inject liquidity, clear arrears, stabilise the sector.

But clearing arrears is not the same as fixing a system.

The Gas Problem Nobody Can Avoid

Nigeria’s grid depends overwhelmingly on thermal generation. Gas-fired plants supply most of the country’s electricity. And gas is not priced in sentimental currency.

For a typical thermal GenCo, gas accounts for about 60 per cent of operating costs. Those gas contracts are effectively indexed to the dollar. When payments are delayed, interest accrues in dollar terms.

This is where the arithmetic turns unforgiving.

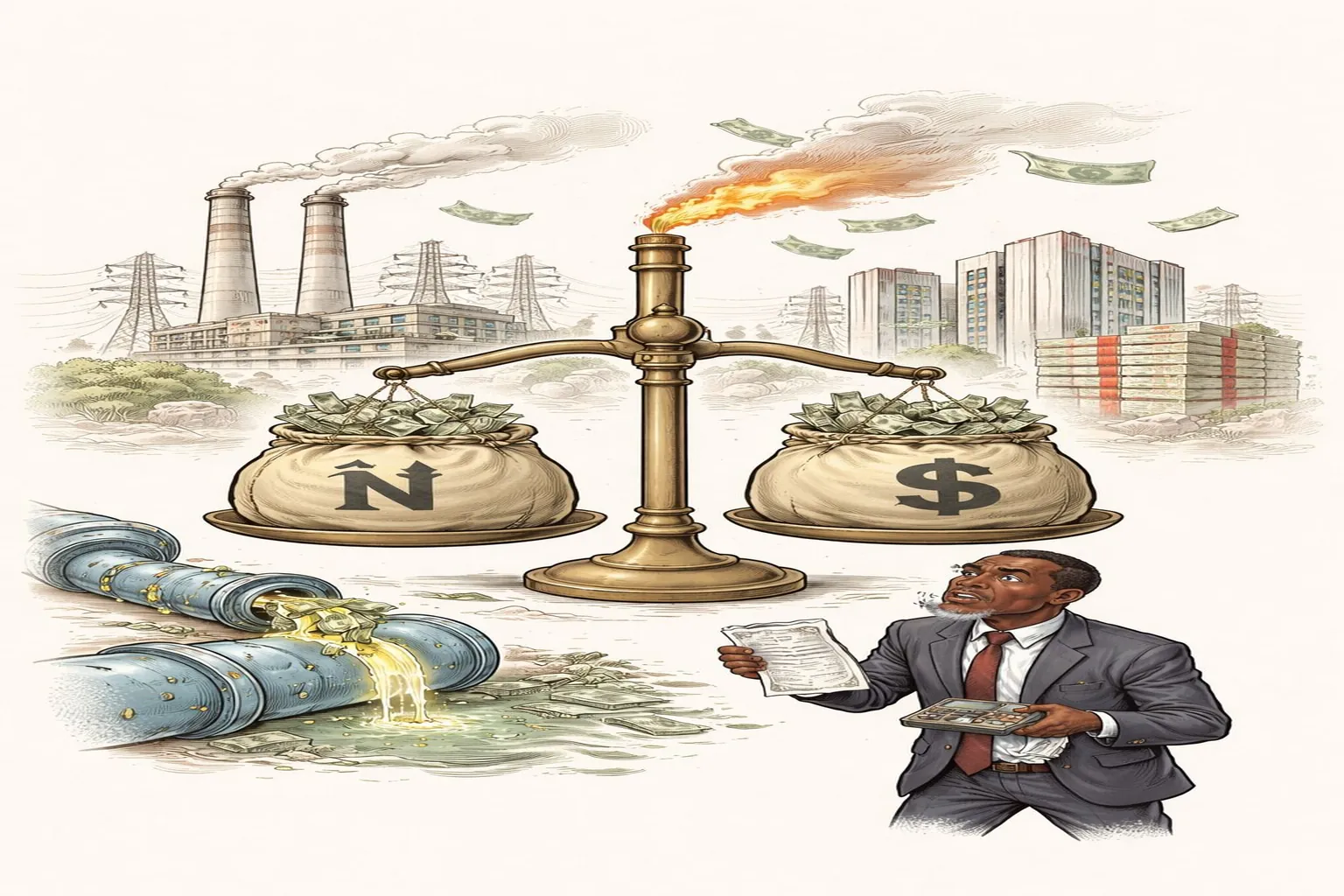

GenCos earn in naira. Their largest cost component is dollar-linked. When the exchange rate is stable, that mismatch can be managed. When the currency collapses, it becomes destabilising.

When the power sector was privatised in 2013, the exchange rate hovered around ₦160 to the dollar. Today, under a market-aligned framework overseen by the Central Bank of Nigeria, the naira trades closer to ₦1,600 per dollar — roughly a tenfold depreciation.

A gas invoice that cost ₦160 million per $1 million obligation a decade ago now costs about ₦1.6 billion for the same dollar amount. Meanwhile, the GenCo still collects only about one-third of its invoiced naira revenue.

The result is a widening gap between what comes in and what must go out.

Why Some Call It “Arithmetically Impossible”

Clark’s argument is blunt: under current conditions, it is mathematically impossible for a thermal GenCo to clear its gas obligations from NBET’s partial naira payments — even if it devoted every kobo collected to gas.

The reason is not ideology; it is compounding.

The principal of unpaid gas invoices has been revalued by exchange rate depreciation. Interest accrues in dollar terms. Domestic inflation erodes the real value of naira collections. Tariff politics limits cost recovery. Payment rates remain below 40 per cent.

The liability grows faster than the cash flow designed to extinguish it.

This, analysts say, explains why some GenCos publicly reject headline settlement figures — whether ₦2.8 trillion or similar political compromises. From their perspective, the true receivable is not simply the nominal naira arrears. It includes capacity payments, gas pass-through costs, FX revaluation effects and dollar interest.

Looking only at naira figures, they argue, creates what Clark calls a “solvency fiction” — the appearance of sustainability without the underlying cash flow to support it.

What the Bond Plan Actually Achieves

There is no doubt the federal bond programme provides temporary relief. It injects liquidity and clears part of the historic backlog. Investors may even welcome the financial engineering.

But critics argue that it does not address the structural contradiction at the heart of the system: naira revenues financing dollar-indexed costs in an environment of chronic under-recovery.

If tariffs do not fully reflect costs, and if exchange rate risk continues to sit on the balance sheets of thinly capitalised generation companies, new arrears will inevitably replace old ones.

A bond can wipe yesterday’s debt from the books. It cannot change tomorrow’s cash flow mismatch.

The Hard Question for Government

Clark’s most uncomfortable implication concerns responsibility. If federal policy insists on dollar-linked gas pricing for the power sector, then the logical primary obligor on those gas contracts, he argues, should be the Federal Government itself — not private GenCos whose balance sheets have already been weakened by years of regulated underpayment.

In simpler terms, if government policy creates the FX risk, government may need to carry that risk.

Expecting private generators to absorb a decade of currency collapse, dollar interest accumulation and tariff constraints — while receiving barely a third of their invoice value — stretches commercial logic.

Until policy explicitly recognises this mismatch, no volume of naira bonds, however well structured, may be sufficient to make thermal generators whole or guarantee uninterrupted gas supply.

Why This Debate Matters

Nigeria’s economic recovery depends on stable electricity. Manufacturers, telecom operators, banks and households all depend on predictable power. When generation falters because gas suppliers are unpaid, the macroeconomic consequences ripple outward — from inflation to unemployment.

The power sector debt debate is therefore not an abstract financial quarrel. It is about whether the foundational numbers of Nigeria’s electricity market are internally consistent.

At its heart, the argument reduces to four variables: naira revenues, dollar costs, chronic underpayment and a tenfold exchange rate shift.

Until those numbers reconcile, the reform narrative may continue — but the arithmetic will continue to resist.