This might be a bit of a long post with lots of background reading but I will try to keep it as quick as possible. First a bit of background. We know that countries can end up with currency mis-alignments especially countries that operate fixed exchange rate regimes. A short read from my old blog on that here. Countries like Nigeria are particularly prone because of the oversize impact of crude oil which still makes up over 85 percent of all exports and somewhere around 65 percent of government revenue. While crude oil prices are “high” we can maintain strong (aka overvalued) currencies but when prices fall we are suddenly faced with two effects: first the actual effect of the shock on inflows of both foreign exchange and government revenue; second, the end of our capacity to maintain that overvalued currency. We see evidence of this problem in trade balances, current account balances, and sometimes the movement in foreign reserves.

The policy question is then twofold: first before the crisis you should be building buffers and making sure that those imbalances are dealt with; second you need flexibility to respond to the crisis once the crisis happens. Either way once the crisis hits you typically have a choice to make: you can choose to save the economy or you can choose to save the currency. A short thing I wrote here.

What do these choices look like in practice? Well luckily we do not have to go too far to see that. In 2014 to 2016 we faced almost the same scenario. Fiscal buffers were weak with the excess crude account (a kind of government savings account for those who are not aware) having only $2bn or so in it. The foreign reserves were healthier though at about $40bn at its recent peak although given oil prices over the previous few years it should have been higher. The oil price crashed to just above $30 a barrel and we made our choices. We chose to save the exchange rate over the economy. We limited sales of foreign exchange to “preferred sectors”. We implemented all sorts of administrative controls on foreign exchange trading. Implemented all sorts of measures to limit imports. Rapidly expanded foreign debt to “reflate the economy”. The list goes on. All these were net negative for the economy of course. The exchange rate survived, officially, for a while but the economy tanked.

There are still those who argue that the recession was really about the fall in oil prices but my opinion is that, while the fall in oil prices played its part, the real culprit was the policy response to the fall in oil prices. A response that chose to sacrifice the economy on the altar of the exchange rate. Of course, once we changed track a bit specifically with a devaluation and a bit more market driven exchange rate the economy started to recover. Unfortunately, we actually did not unwind most of the negative administrative measures instituted. But at least the collapse stopped.

Unfortunately, as these things go, we went back to the old habits of choosing the exchange rate again. Keeping it fixed against the dollar regardless of the macroeconomic fundamentals.

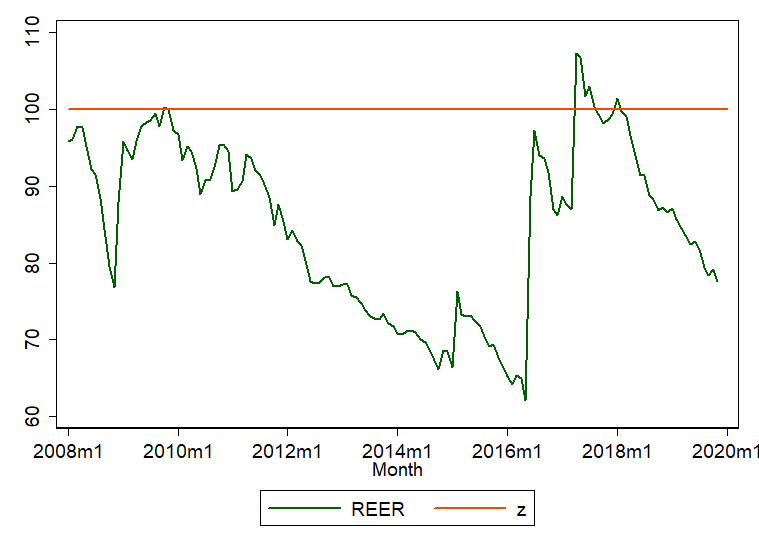

As you can see from the chart above which is from the CBN, the exchange rate has been creeping up in real terms since about 2018. The chart is a bit outdated but by now it is probably almost as overvalued as it was before the 2014 oil price crash hit. This time around the CBN did not maintain this with large foreign inflows from extra high $100 oil like it did before 2014. This time it maintained this via a constant squeeze on the economy selling high interest rate instruments (OMO bills) to foreign portfolio funds and keeping interest rates high for most of the economy at least until recently. Supporting the border closure to suppress imports and doing all sorts to limit demand for foreign exchange. Etc. If you have been reading my previous monthly updates then this is no news to you. This has been very expensive of course. The squeeze on the economy was significant enough that even it has had to try to change tactics. It has tried to force interest rates down by essentially splitting the securities markets into two: a high interest one for foreign portfolio funds and a low interest one for Nigerians while at the same time using tactics to force banks to lend. While still trying to maintain its fixed exchange rate peg. A kind of eating its cake and having it.

These inconsistencies have of course been problematic and the market has been voting with its feet for some time.

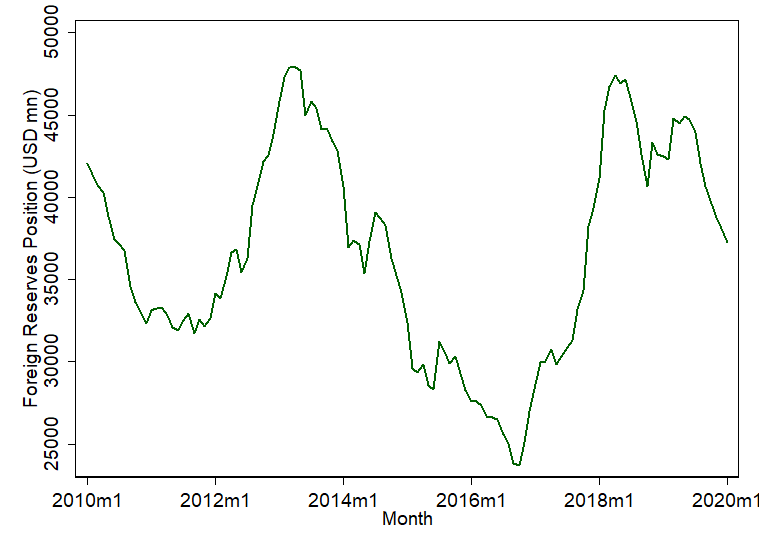

Since about 2018 the reserves have been on a downward trajectory. As at writing this it was just over $36bn. And remember that includes the amount that is indirectly owed to FPIs who can exit relatively quickly.

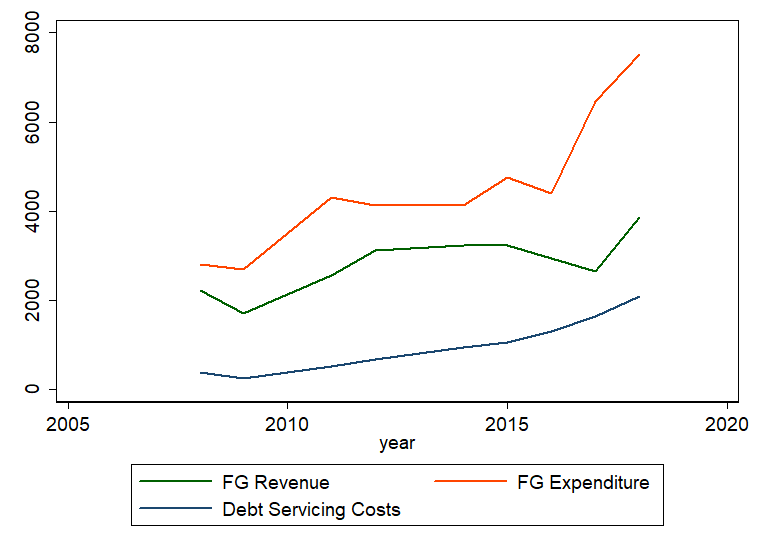

On the fiscal side the government has continued to spend at will and raise debt at will.

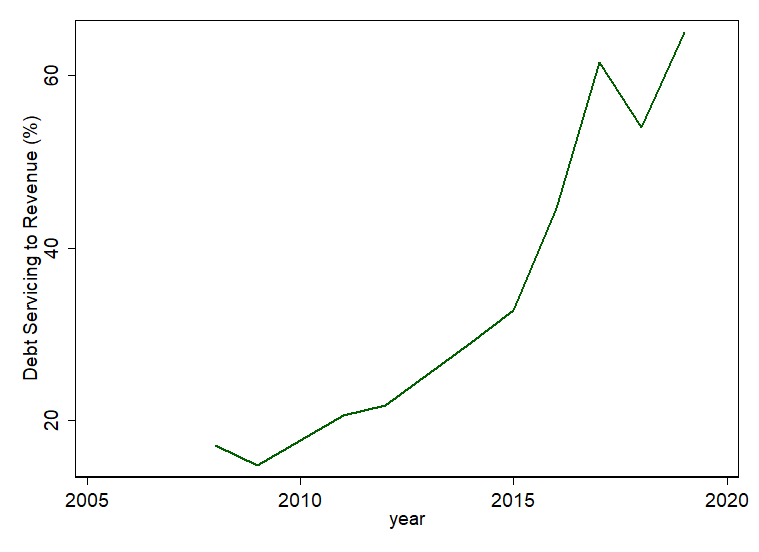

Revenue has increased a bit but the growth of spending has been way faster. As a result debt servicing costs have climbed significantly so much so that in 2019 almost 65 percent of all revenue was spent just servicing debt.

The fiscal imbalances are so severe that recurrent expenditure in the 2020 budget is 80 percent larger than the actual revenues in 2019. And of course the fiscal buffers have essentially disappeared. The excess crude account was down to $72m as at last month. The Sovereign Wealth Fund has some funds ( $1.5bn as their last annual report in 2018) but much of that is tied to illiquid infrastructure projects. The stabilization fund component was about $390mn only as at the end of 2018. The NSIA used to publish quarterly results but have not done so since 2017. So we don’t know the value of the fund now but I doubt it is that large. Summary: no real fiscal buffers.

The room for using debt to ease the crisis are also limited. For context if you compare Nigeria’s actual debt to revenue ratio it looks close to that of Greece during their debt crisis and is larger than the other PIGS countries during the EU debt problem in 2015.

So the debt option is kind of closed.

Morale of this whole story: on the two key vulnerable points for the Nigerian economy, exports (foreign exchange inflows) and government revenue, the policy direction was largely unsustainable even before this oil price collapse. The question for most was when all this unsustainability would mature. When the bubble would pop.

And so.. oil prices have collapsed again and essentially we are back to the 2014-2016 problem. The exchange rate or the economy. Before the crash the imbalances were already building up. So what options do we have now that the crash has happened? The difference this time around is that we already have many of those choosing-the-exchange rate policies in place. We already have a 41 items restriction list (or is it 42?). We already have the borders closed. We already have a high debt build up. We have already borrowed foreign reserves from FPIs. We have already squeezed banks. We have already sold FX futures.

The fundamental choice is back again: exchange rate or economy? So far it looks like we will be choosing the exchange rate again. Unsubstantiated rumours suggest the president told the economic advisory council that he doesn’t even want to hear anything about the exchange rate. The CBN is already releasing press statements on how the exchange rate is appropriately priced and threatening fire and brimstone on currency hoarders. EFCC is already attacking BDCs. All signs point to a repeat of 2014-2016 where we did all we could to choose the exchange rate until the economy fell into recession.

Markets are also already responding. The stock exchange has lost all its gains this year and is 24 percent down since its peak in mid-January. The black market is flashing signals with rumours of exchange rates as high as 400 naira per dollar. Nigeria’s Eurobond rates have increased from 7 to over 10 percent.

How far will it go? The damning thing is no one knows. It all depends on how a couple of people feel when they wake up in the morning. And that part is largely unpredictable. But if we repeat the policy choices we made in 2014 to 2016 then the outcomes will be worse. Because we have much less room to maneuver this time around. And there is much less optimism. Hold on to your hats, its bound to be a bumpy ride.

Caveat: oil prices could rebound to $100 and the corona virus pandemic could disappear tomorrow. But even that may not prevent the unwinding that is to come.

Dr. Nonso Obikili is a Policy Associate at Economic Research Southern Africa. Click here to subscribe to his monthly updates.

Culled from Nonso’s Nigeria Economic Update