Recent slides in the official exchange rate of the Naira and the dramatic widening of the parallel market premium signaled that the unease in the Nigerian foreign market has intensified, testing our capacity as a nation to stabilize the Naira. This piece simplifies the forces at work and identifies fruitful paths to a stable Naira.

- Crucial Role of Pandemic-Related Trade Shocks

We must remind ourselves that the current exchange rate crisis is triggered by the foreign exchange supply shortfalls in the wake of the pandemic induced global lockdown in 2020.

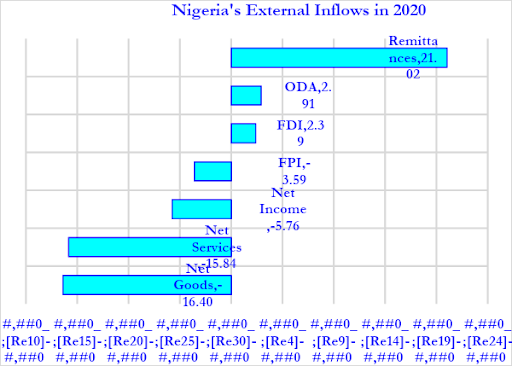

Source: 2020 Statistical Bulletin, Central Bank of Nigeria.

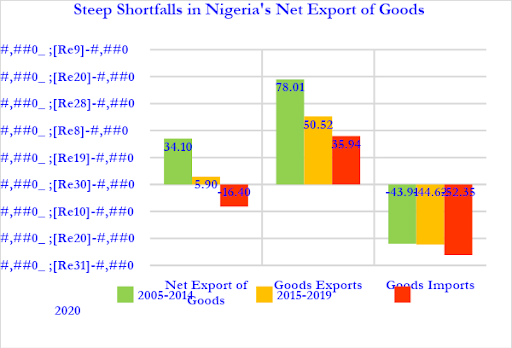

- Nigeria’s annual average net goods exports inflow of US$34 billion from 2005 to 2014 had dropped to an annual average inflow of US$5.9 billion from 2015 to 2019, before dipping steeply into steep net outflow of -US$16.4 billion in 2020 (that was a US50 billion shortfall relative to the 2005-2014 average) and it is likely to remain a net outflow in 2021.

- Balances on Nigeria’s trade in services and incomes have historically been negative.

- Remittances is now the only source of net inflow on Nigeria’s current account, with annual average inflow of US$21 billion from 2005 to 2020. This was not large enough to offset deficits from goods, services, and income, leaving the current account in a steep deficit of -US$16.98 billion in 2020.

- The combined FDI and ODA inflows of about 5.2 billion were offset by FPI outflows of 3.6 billion to leave net capital inflows at a paltry 1.7 billion in 2020.

Nigeria’s external payments situation is unlikely to change much in 2021 as we have done nothing to reposition to attract the types of the liquidity inflows that are abundantly available in the prevailing global environment like many of our peers are already doing as shown below.

Also Read: Insights on Value Added Tax (VAT) Collection and Distribution in Nigeria

- The Role of Supply

Overall foreign exchange supply conditions are determined in part by:

- Generic developments in external trade and payments conditions that have reduced net-inflows of foreign exchange into Nigeria, and indeed all other countries.

- Government’s capacity to boost the sizes of net-inflows from targeted components of the current and capital accounts, especially in the face of pandemic-related downswings in global economic conditions that helped some countries blunt the edges of adverse generic shocks.

- Confidence or lack of confidence of residents and non-residents in the ability of the government to stabilize supply in the event of adverse shocks could inform their decisions on whether to hoard or sell foreign exchange, especially in the face of crisis.

- The Role of Demand

Demand conditions are determined by

- Transactions’ demand to meet routine external trade and financial obligations, could largely be procyclical

- Precautionary demand to meet unexpected external trade and payments obligations, would increase in times of uncertainty.

- Speculative demand to seize external investment or portfolio optimization opportunities, would explode in times of uncertainty.

- Exchange Rate as An Indicator

The Naira exchange rate against the US dollar is a mirror that helps us to track how good we look in ensuring adequate levels of foreign reserves to meet readily foreseeable transactions demand for forex required for routine external payments, not-so-foreseeable precautionary demand required to cope with unexpected external shocks, and largely unforeseeable speculative demand required to seize external investment and portfolio optimization opportunities.

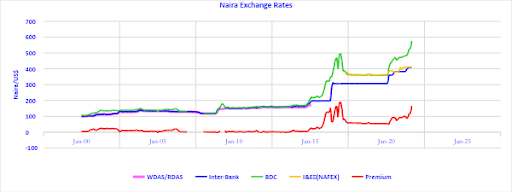

We looked and felt very good in front of that mirror when our external reserve situation improves steadily to stay well above the US$35 billion, like 2006 to 2014, often affording ourselves some boasting rights on how successful our economic policies had been.

Conversely, we looked and felt very bad in front of that mirror when our external reserve situation deteriorates precipitously to drop below US$35 billion like 2015 to 2017 when the Naira fell precipitously from 120/US$ to 360/US$, and 2020 to 2021 when it fell further to 410/US$ in official wholesale market segment, and US$575 in unofficial retail market segment, often pushing us to live in denial, try to obstruct access of buyers and/or retail dealers to foreign exchange market, try to cover the mirror, break the mirror, or even blame market operatives for the woes.

Shortfalls in foreign exchange supply, or foreign exchange reserves, relative to demand are the most common fundamental sources of exchange rate instability, although confidence-related demand shocks are known to have triggered exchange rate crisis even in the absence of supply shortfall or aggravate crisis that originally broke out because of supply shortfalls.

The exchange rate is a mere indicator of the balance of supply and demand forces in the foreign exchange market. Those who are discussing exchange rate developments without reference to the unfolding realities of demand and supply are chasing the shadows instead of substance.

- Exchange Rate Premium is Informative

Wherever governments try to cover up supply shortfalls by pegging the official exchange rate at a value that does not equate supply with demand, gaps, spreads, or premiums emerge between rates in official and parallel market segments. These premiums are very informative when the market is out of equilibrium as they largely reflect the size of the supply shortfalls or the distance of pegged exchange rate from market realities. The trend of the premium reveal useful news which no market participant can afford to ignore. Policies should be guided by them, rather than ignore, or suppress that news.

- How we should address the crisis

Increasing foreign exchange supply is the only enduring way to narrow or close premiums. We should learn that it is just as futile to try to curtail demand for forex as it is to try to control the price of forex. Supply of forex is the only variable that we should be trying to boost.

The sooner we refocus our efforts on how to substantially boost foreign exchange supply in Nigeria, through balance-sheet-related foreign exchange inflows that are fueled by the unprecedented global liquidity glut, rather than transactions-related foreign exchange inflows that are adversely affected by weakening global commodity prices, the better.

Most other oil exporting developing countries have shifted from relying on oil exports for foreign exchange supply towards asset-based securities that is helping them to attract bigger net foreign exchange inflows than oil could ever have brought even in the best of times.

Fighting over exchange rate premium distracts us from concentrating on how to raise large sums from global asset-based securities like progressive developing countries are doing.

Also Read: Finding a Way Out of Nigeria’s High Debt Costs

- Connecting to Global Wave of Asset-Linked Securitization

Opportunities for issuing asset-based securities that will connect global liquidity into local assets internationally, other countries are seizing heavily on these opportunities, but Nigeria continues to shun such opportunities by focusing on exchange rate and demand-side participants rather than how to boost supply.

Global wave of asset-linked securitization increasingly converts dead, idle, and underutilized public corporate, infrastructure, physical, and intangible assets into new sources of immediate fiscal liquidity and future revenue flows that are required to close infrastructure gaps and unlock latent growth potentials, without the burden of interest payments through the budget, as commercial investors in such securities are happy to wait for the profits or rent to be unlocked by the assets, mostly at their own risk, with the comfort that most of such securities have investment grade ratings by foremost agencies.

- The Way Forward

We should create special purpose vehicles for packaging infrastructure assets for big-ticket interest-free financing through asset-linked non-convertible or convertible bonds. The gains of India and a few other countries who have learnt to attract record levels of foreign capital inflows by issuing asset-based bonds targeted at their diaspora, the breakthroughs of China, Brazil, India, and a few other developing countries in leveraging on local assets to receive record levels of global equity inflows through cross-border mergers and acquisitions and greenfield deals, and the successes of Malaysia, Saudi Arabia, and about six other oil producing countries in issuing interest-free commercial bonds to replace interest paying ones, all show that Nigeria’s options for boosting non-oil, non-export liquidity in the prevailing global milieu are endless!

naira naira

-

-

-

-